Verizon reports that 31% of breaches now start with software vulnerabilities, and 48% involve ransomware. For financial services teams, those numbers show up as production systems with unclear owners, critical findings aging in queues, stale audit evidence, and third-party dependencies nobody can fully map.

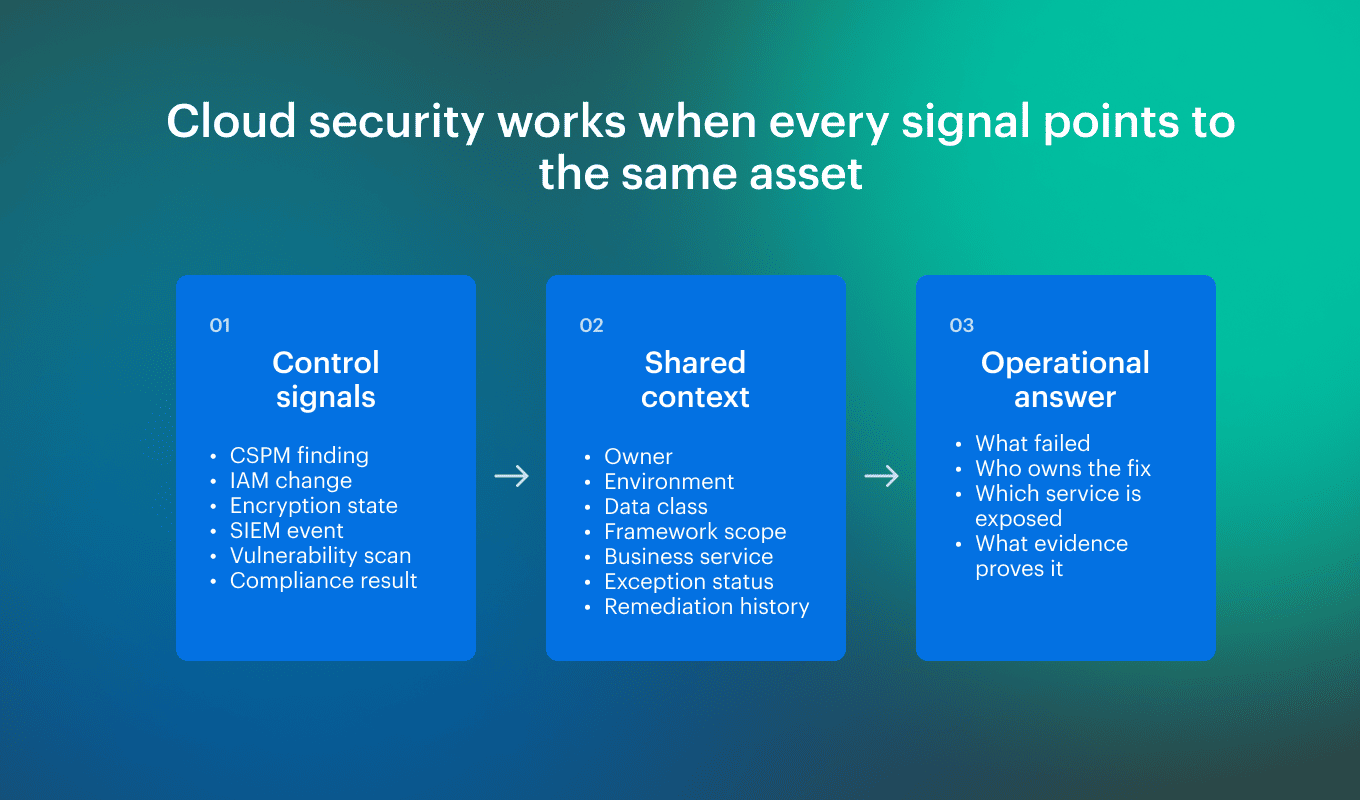

That is where cloud security for financial services gets hard. A failed CSPM control, vulnerability scan, SIEM event, or CMDB record only helps if it carries the context engineers need: owner, environment, data class, framework scope, exception status, business service, and remediation history.

This guide explains how to build financial services cloud security as a control-evidence system, covering:

- Which 2026 regulatory requirements change day-to-day cloud security work

- Where cloud security programs fail across inventory, ownership, controls, and evidence

- How to structure evidence architecture so teams are not rebuilding proof before every audit

- How to handle vulnerability ownership, storage controls, identity context, and scope drift in regulated cloud environments

- How to map SaaS, cloud provider, and third-party dependencies to critical services

- Which metrics show whether the program is working

Key insights

- Financial services cloud security now fails at the evidence layer, not the control catalog. 31% of breaches now start with software vulnerabilities, and 48% involve ransomware (Verizon). For cloud teams, the operational question is whether the finding can be tied to the affected asset, regulated service, owner, and evidence trail.

- One cloud asset can trigger several review paths at once. A payment database, customer data store, or SaaS-connected workload may fall within the scope of PCI DSS, SOC 2, FFIEC, GLBA, SEC, or DORA. Treat those frameworks as different evidence consumers.

- Financial institutions need dependency evidence for KYC, AML, identity, payment, market data, and SaaS-supported workflows. 55% of financial services respondents identify third-party risk as their greatest cloud security threat (CSA), while 44.5% of observed cloud intrusions used third-party software-based entry (Google Cloud).

- Data class changes the control question. A public dev bucket, payment tokenization store, claims repository, trading dataset, backup vault, and AI ingestion dataset may all look like storage in the cloud console. They do not need the same evidence, retention, encryption, or access review path.

- The useful metrics prove ownership, freshness, and closure. Raw finding counts and pass rates can hide unscoped assets, missing logs, expired exceptions, and resources nobody owns. Stronger metrics include unowned cloud assets, evidence freshness, vulnerability age by business service, exception age, and remediation SLA breaches.

What is cloud security for financial services?

Cloud security for financial services is the set of technical controls, governance processes, monitoring practices, and audit evidence used to protect regulated financial workloads, customer data, payment systems, and third-party cloud dependencies across public cloud, SaaS, and hybrid environments.

Financial institutions already have plenty of security signals: CSPM findings, IAM changes, encryption states, SIEM events, vulnerability scans, and compliance reports. The problem starts when those signals do not point to the same asset, owner, business service, and evidence trail. A regulated workload needs context:

A regulated workload needs context:

- Which cloud account, subscription, project, tenant, cluster, or SaaS environment contains it

- Which owner and support group are accountable for it

- Whether it is production, non-production, internet-facing, or internal

- Whether it touches cardholder data, NPI, PII, trading data, claims data, logs, backups, or derived analytics

- Which framework or internal policy applies

- Whether a failed control is open, remediated, or accepted as an exception

- Whether the evidence is current enough for audit, incident response, and operational risk review

Why financial services cloud security needs asset-level evidence

The difference is that financial services teams have to prove not only that something failed, but also which regulated service, customer data flow, third-party dependency, and control obligation it touched.

Reason 1. The same cloud asset can fall under several evidence regimes

DORA applies to 20 types of financial entities and ICT third-party service providers, PCI DSS applies to payment account data environments, and public companies may need to disclose material cybersecurity incidents within four business days after materiality is determined.

That is why a cloud finding needs owner, environment, data class, framework scope, control result, timestamp, and remediation record. Without those fields, the team cannot tell whether the issue is an engineering backlog item, audit evidence gap, reportable event, or regulator-facing risk.

Reason 2. Third-party dependencies are part of the risk surface

CSA’s 2026 financial services cloud and AI report found that 55% of respondents identify third-party risk as their greatest cloud security threat. Google Cloud’s H1 2026 Threat Horizons report found that 44.5% of observed cloud intrusions used third-party software-based entry.

In fintech and banking environments, a finding needs to show whether the affected asset connects to a KYC vendor, AML platform, identity provider, payment rail, market data feed, cloud service, or SaaS system supporting a critical workflow.

Reason 3. Customer trust has evidence requirements attached to it

IBM’s 2025 breach research puts the global average breach cost at $4.44 million, while the U.S. average reached $10.22 million.

In financial services, the evidence record has to support more than incident cleanup. It may need to show what data was involved, which customers or services were affected, who owned the response, whether the control gap was closed, and which records support compliance review, customer notification, or disclosure analysis.

Why cloud security evidence differs across financial services organizations

Financial services organizations carry risk concentration that most generic enterprise cloud programs do not face.

| Organization type | Typical cloud security pressure | Evidence that usually matters |

|---|---|---|

| Fintech | Customer and partner assurance, SOC 2 Type II, PCI DSS, fast release cycles | Access reviews, production change evidence, vulnerability age, control operation over time |

| Bank | FFIEC IT Examination Handbook expectations, operational resilience, third-party risk | Technology inventory, architecture controls, incident/recovery evidence, vendor and cloud dependency mapping |

| Insurer | Privacy, retention, claims systems, legacy dependencies, backup/recovery | Data location, access paths, retention, backup evidence, incident history |

| Payment processor | CDE scope, card networks, segmentation, tokenization, transaction availability | CDE-tagged assets, segmentation evidence, logging status, vulnerability records, encryption state |

| Asset manager | Trading systems, market data, latency-sensitive workloads, settlement systems | Service dependency maps, integrity controls, privileged access, resilience evidence |

The stack is also more interconnected. KYC providers, fraud platforms, payment gateways, SWIFT integrations, FedNow connections, card networks, identity providers, SaaS admin tools, market data feeds, and managed databases all become part of the security surface once they support production workflows.

The regulatory stack financial services cloud teams actually face

Financial data security in the cloud usually sits across several frameworks at once and these frameworks are not interchangeable. Control overlap does not mean one test satisfies every framework. It means the same evidence object can be reused when scope, timestamp, control intent, and reviewer expectations are preserved.

| Framework or regulation | Who it usually affects | Cloud security focus |

|---|---|---|

| PCI DSS 4.0.1 | Payment processors, fintechs, merchants, issuers, acquirers, and entities storing, processing, or transmitting payment account data | CDE scope, access, logging, vulnerability management, segmentation, payment account data protection |

| SOC 2 Type II / SOC 1 | Fintechs, SaaS providers, processors, B2B financial platforms, and service organizations | Security, availability, confidentiality, privacy, processing integrity, and financial-reporting controls where SOC 1 applies |

| FFIEC IT Examination Handbook | US banks, credit unions, and regulated financial institutions examined by federal banking regulators | Architecture, infrastructure, operations, technology risk management, resilience, third-party service dependencies |

| GLBA / FTC Safeguards Rule | Covered financial institutions under FTC jurisdiction, including many non-bank financial services firms | Customer information protection, information security program, risk assessment, safeguards, service provider oversight |

| SEC cybersecurity disclosure / Regulation S-P | Public companies, broker-dealers, investment advisers, funds, transfer agents, and other SEC-regulated entities where applicable | Material cybersecurity incident disclosure, customer information safeguards, incident response, service provider oversight, recordkeeping |

| DORA, where EU operations apply | US financial institutions, fintechs, asset managers, insurers, or service providers with EU-regulated operations or ICT dependencies | ICT risk management, operational resilience, incident reporting, ICT third-party risk, critical functions |

The table above focuses on the frameworks most likely to change cloud evidence work for US financial services teams. DORA, OSFI B-13, MAS TRM, FCA guidance, GDPR, and other non-US requirements still matter for firms with global operations, but they should be treated as overlays.

Read also: Cloud Data Security Best Practices - A Playbook for Multi-Cloud and Migration

Why financial services cloud security fails in real environments

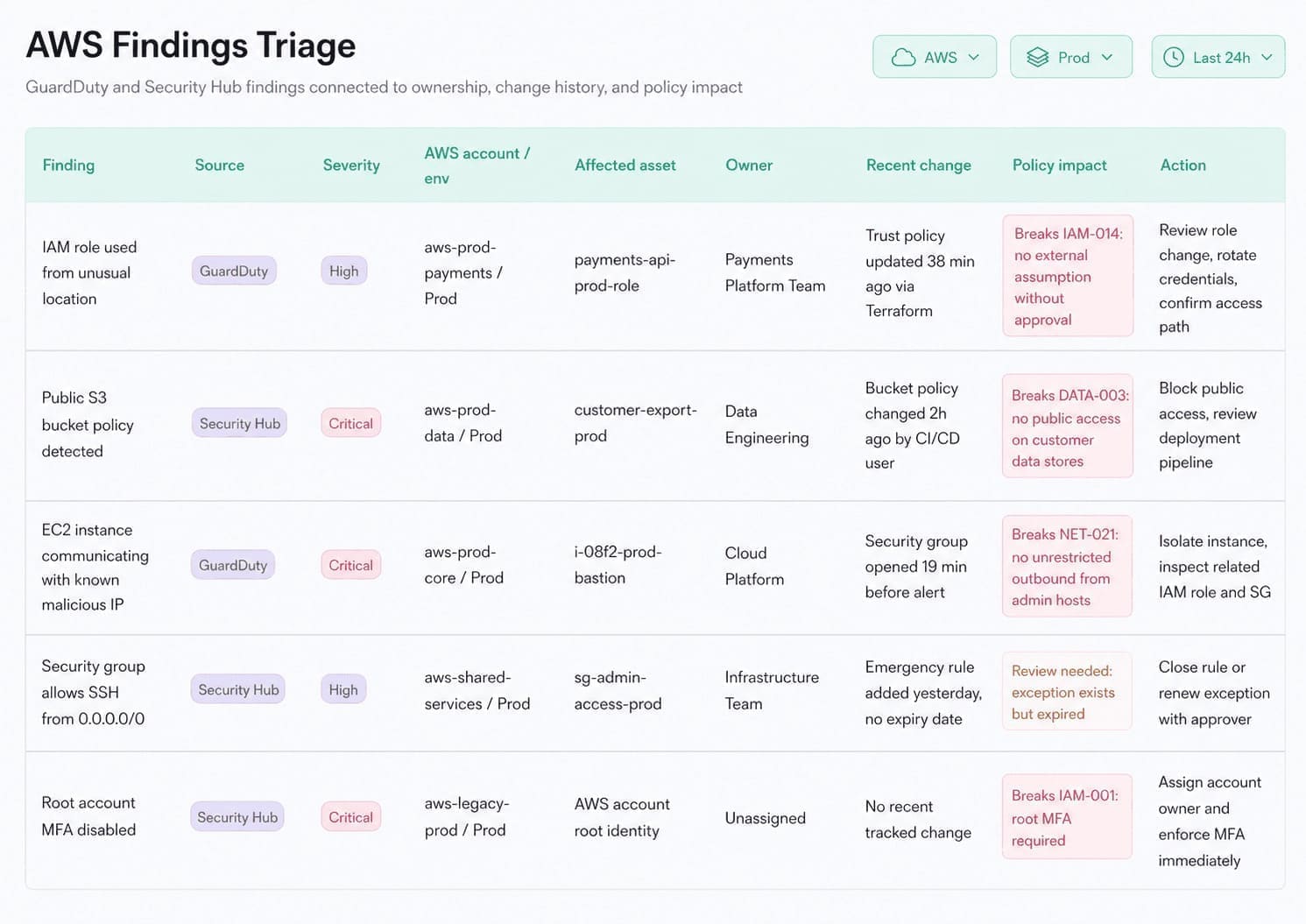

Picture a fintech security team after a scan: CSPM says a storage bucket is public, the CMDB knows the cloud account, and Jira has a ticket in a shared queue. But the missing part is whether the asset touches customer PII, cardholder data, a payment flow, or a critical third-party service.

Across Cloudaware client environments, Katerina L., Cloud Security Expert, sees the same pattern: financial services security starts to fail when every tool holds a fragment of the answer, and no record connects the asset to ownership, scope, service impact, and evidence history.

CSA’s report found that 20% of organizations have experienced AI-related security incidents, while another 21% are not sure whether such incidents occurred. IBM reports that breaches linked to shadow AI added up to $670,000 to average breach cost and exposed customer PII and intellectual property.

That uncertainty matters because AI agents, service accounts, SaaS access, and data movement all create activity that must be tied back to assets before detection becomes usable evidence. The failure usually appears in four places:

- Ownership: The alert is real, but nobody can see the application owner or SLA

- Evidence age: The screenshot says encryption passed last month, but the resource changed yesterday

- Scope drift: A dev dataset receives production PII, a SaaS integration touches customer records, or an acquired account never enters PCI or GLBA scope

- Dependency mapping: KYC, AML, identity, payment, and market data systems support production workflows but are not connected to the affected asset

“The CMDB model is what saves you in this situation. If the finding already carries owner, application, data scope, exception status, and ticket history, security can answer the question instead of rebuilding the investigation every time compliance, engineering, or an auditor asks what happened.” — Katerina L., Cloud Security Expert at Cloudaware Cloudaware connects the failed control to the asset, owner, service, exception, and ticket history, so the finding can move from detection to remediation evidence.

Cloudaware connects the failed control to the asset, owner, service, exception, and ticket history, so the finding can move from detection to remediation evidence.

For the broader threat landscape, see the cloud security threats guide.

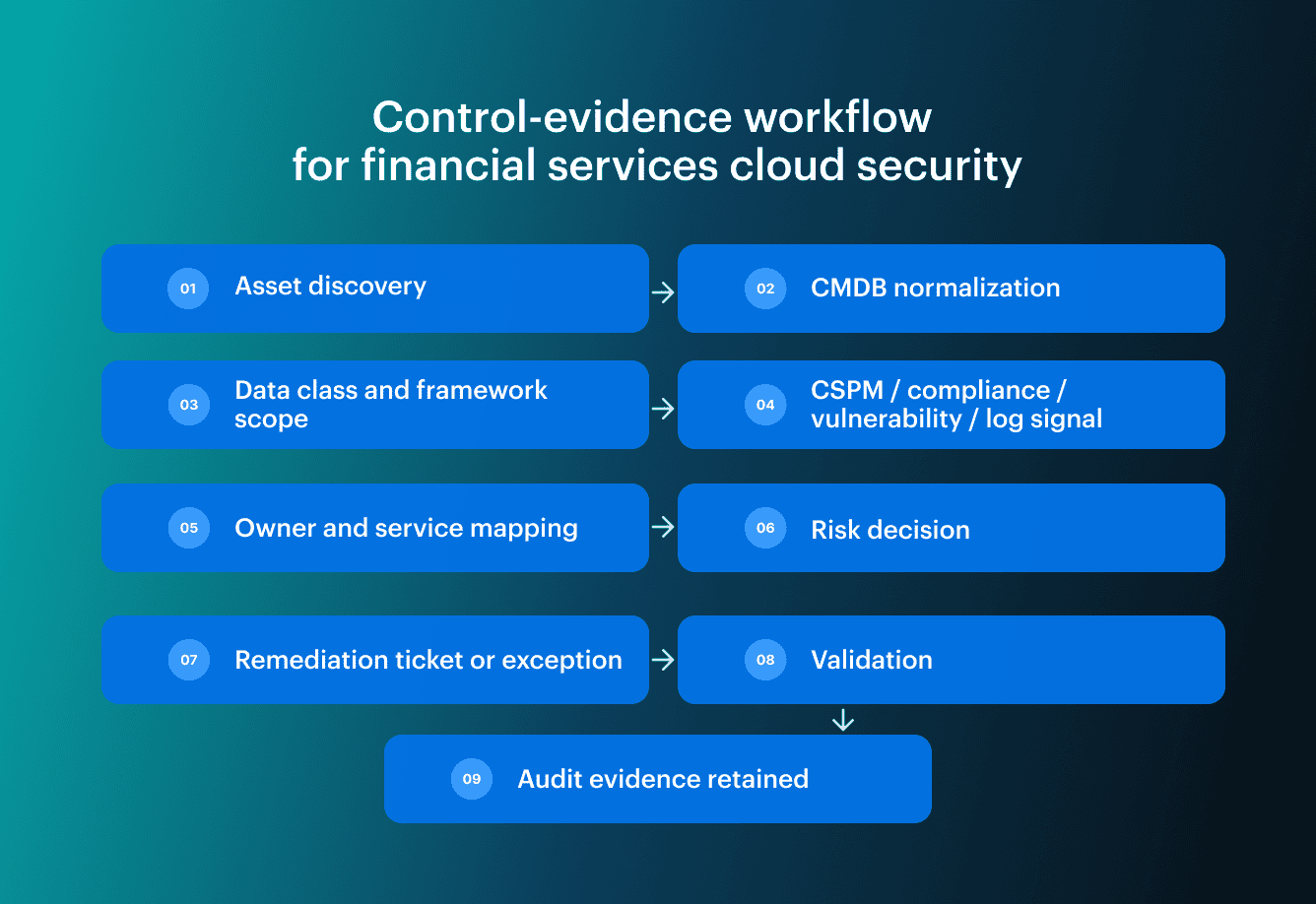

How financial services cloud security teams keep evidence current

Financial services cloud teams can operate at scale when posture management, audit evidence, and remediation stop moving through separate tracks. The working pattern starts with asset discovery, but it only holds if the evidence stays attached through scope, control evaluation, remediation, exception handling, and validation. The workflow only holds if the inventory carries the right fields. AWS accounts, Azure subscriptions, GCP projects, Kubernetes clusters, databases, storage, IAM roles, service principals, SaaS dependencies, network objects, VMware assets, and security tooling coverage all need the same operational context.

The workflow only holds if the inventory carries the right fields. AWS accounts, Azure subscriptions, GCP projects, Kubernetes clusters, databases, storage, IAM roles, service principals, SaaS dependencies, network objects, VMware assets, and security tooling coverage all need the same operational context.

At a minimum, the record should show:

- Asset identity: Provider ID, account, subscription, project, resource type, and region

- Ownership: Application, service owner, support group, and business unit

- Environment: Production, non-production, sandbox, and DR

- Data class: Cardholder data, NPI, PII, logs, backups, trading data, or claims data

- Framework scope: PCI DSS, SOC 2, FFIEC, GLBA, DORA, where applicable, and internal policy

- Workflow state: Ticket, exception, approval, SLA, remediation status, and evidence timestamp

Exceptions need the same discipline. A temporary exception without an expiration date is just permanent risk wearing a fake badge. A usable exception record should include the failed control, asset owner, risk owner, reason, compensating control, approval, expiration date, retest date, ticket link, and closure evidence.

Remediation also has to land with the team that owns the service. A ticket should carry the asset, owner, exposure, affected business service, framework scope, SLA, validation result, and closure evidence. Otherwise, security has detected a risk and successfully mailed it to nowhere.

Read also: How to Perform a Cloud Security Risk Assessment in 2026

Data protection and cloud storage controls for financial workloads

Financial data security in the cloud starts with data classification, but the value is not the label itself. The value is knowing when the label changes the control question.

A public dev bucket, customer statement archive, payment tokenization store, claims repository, trading dataset, AI ingestion dataset, and backup vault may all look like storage in the cloud console. They should not produce the same evidence.

| Data or storage context | Control question | Evidence to keep current |

|---|---|---|

| Cardholder data or payment account data | Is the resource inside PCI DSS scope? | CDE tag, encryption state, access control, segmentation evidence, logging status, vulnerability record |

| Customer PII or NPI | Can the team prove access, location, retention, and disclosure controls? | Owner, region, access paths, retention policy, encryption state, backup location, exception status |

| Trading, settlement, or claims data | Would integrity, latency, or availability affect a regulated workflow? | Application owner, business service, replication path, backup validation, recovery test, change history |

| Logs and backups | Do they contain sensitive identifiers or regulated records? | Data class, access logging, retention period, encryption, restore evidence, deletion policy |

| AI ingestion or analytics datasets | Can the team prove which source data entered the model or workflow? | Source system, data class, approved use, access path, retention, owner, review record |

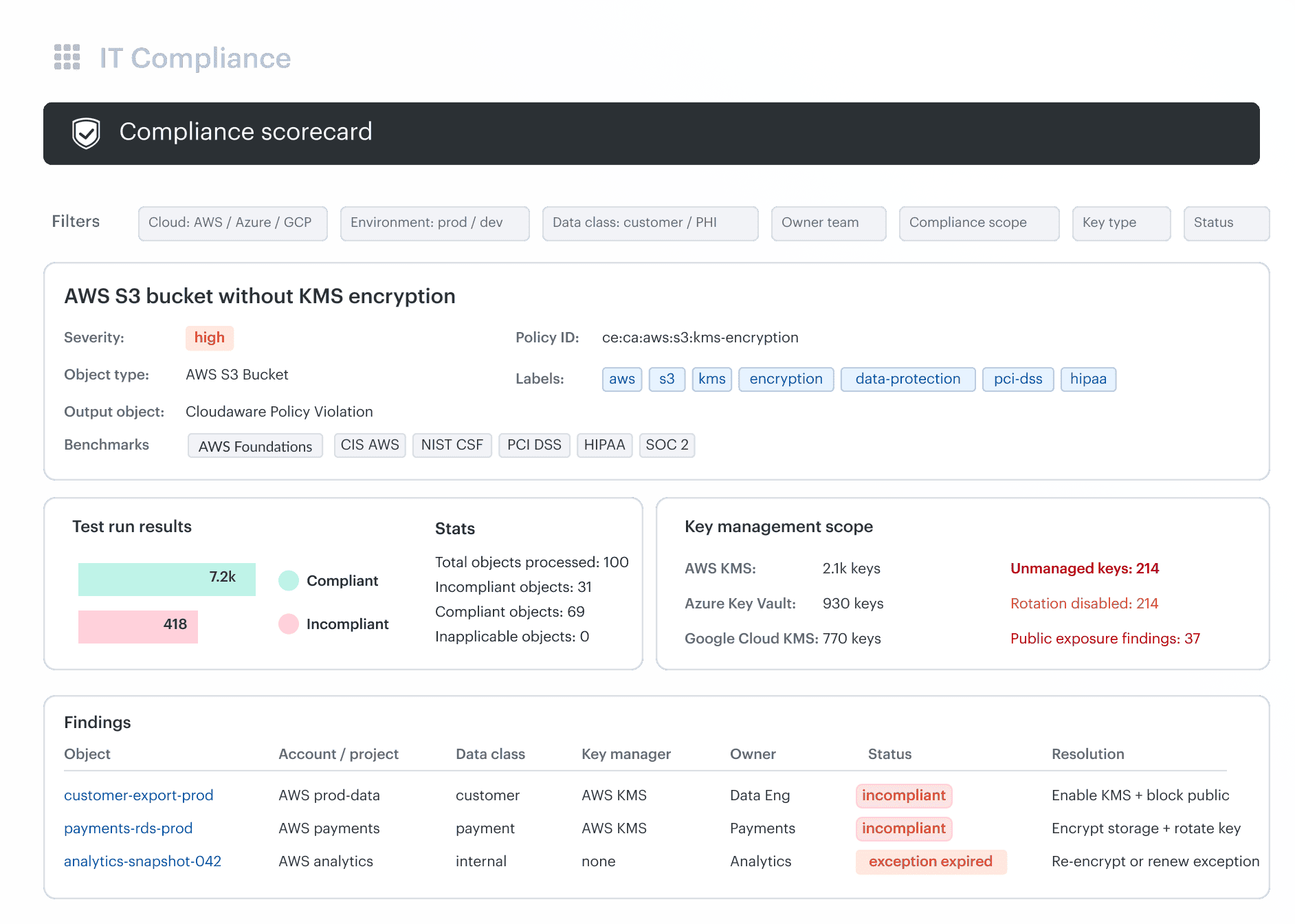

Cloud storage financial data security measures should produce evidence that an engineer, auditor, or incident responder can test. Each regulated storage record should show who owns it, what data it holds, how it is protected, and whether the latest control result is still current.

PCI DSS is a clean example: before the team can prove payment account data is protected, it has to identify the cloud resources that store, process, or transmit it. Scope comes before control proof. Example of Cloudaware’s UI showing storage encryption status, KMS coverage, data class, owner, compliance scope, and remediation action in one evidence record.

Example of Cloudaware’s UI showing storage encryption status, KMS coverage, data class, owner, compliance scope, and remediation action in one evidence record.

Third-party, concentration, and operational resilience risk

Third-party cloud risk is not solved by vendor due diligence. A questionnaire tells you what a provider claims. Operational resilience needs to know what breaks when that provider, region, API, identity service, or managed database is unavailable.

The failure usually appears before an outage, but nobody sees it yet. A payment service depends on one identity provider. A KYC workflow relies on one SaaS platform. A fraud model reads from a managed database in one cloud region. The architecture diagram shows redundancy, while the live dependency map tells a different story.

DORA made this visible in Europe by turning ICT third-party risk and operational resilience into explicit supervisory concerns. For US-centered financial services teams, DORA is still useful as an operating reference when global operations, EU customers, or ICT provider dependencies are involved.

A resilience review should show:

- Which business services depend on one provider, region, SaaS platform, API, queue, or database

- Which critical functions would be affected by an outage or degraded provider service

- Which recovery path exists, including RTO, RPO, backup validation, and failed-test remediation

- Which open findings, exceptions, or dependency risks still affect the service

- Which evidence proves the dependency is known, reviewed, and controlled

“The third-party risk conversation changes once a SaaS provider or cloud service becomes part of a regulated workflow. At that point, a questionnaire is not enough. The institution needs to know which services depend on that provider, what breaks if it is unavailable, and which evidence proves the dependency is controlled.” — Mikhail M., General Manager at Cloudaware

Metrics that show whether the program is actually working

A financial services cloud security program should not be measured by finding volume alone. Raw counts show scanner activity, not control execution. A high pass rate can hide the same problem in a cleaner outfit: unscoped assets, missing log sources, unsupported regions, expired exceptions, and resources nobody owns.

Useful metrics answer a harder question: can the team prove risk is owned, scoped, current, and moving toward closure?

| Metric | What it proves | Useful breakdown |

|---|---|---|

| Unowned cloud assets | Remediation and audit accountability have a real owner | Provider, account, business unit, environment |

| Unscoped regulated assets | Scope drift is visible before audit or incident response | Data class, owner, environment, framework |

| Evidence freshness | Audit evidence still reflects the current asset state | Framework, control, asset, timestamp |

| Open policy violations by age | Failed controls are being worked, not only detected | Owner, severity, business service |

| Exception age and expiration rate | Accepted risk is reviewed instead of becoming permanent | Control, approver, expiry, compensating control |

| Critical or high vulnerability age by service | Material vulnerabilities are tied to business impact | CVE, exposure, owner, service criticality |

| Scan and logging coverage | Regulated assets are actually monitored and assessed | Provider, environment, asset class, log source |

| Third-party dependency coverage | Critical services have mapped provider dependencies | Provider, critical function, region, service |

| Remediation SLA breach rate | Owners close findings within expected timelines | Owner, severity, ticket status |

Evidence freshness matters for the same reason. A control that passed 90 days ago may not help if the resource changed yesterday. The metric should show when evidence was collected, what asset it applies to, which framework it supports, and whether a later change invalidated it.

Read also: A 2026 Practitioner Guide to Cloud Security Vulnerabilities

Cloudaware turns cloud findings into audit-ready evidence

Cloudaware supports financial services cloud security by making the CMDB the join point between cloud inventory, control results, vulnerabilities, logs, exceptions, owners, and tickets.

It does not replace every SIEM, cloud-native control, scanner, or audit process. Its role is narrower and more useful: keep cloud findings connected to the asset context teams need to prioritize, remediate, and prove what happened. Core capabilities:

Core capabilities:

- Unified asset context: Discovers and normalizes multi-cloud and hybrid infrastructure, then ties each asset to the operational context needed for ownership, scope, and investigation.

- Standards and audit evidence: Keeps cloud control evidence tied to live infrastructure, so PCI DSS, SOC 2, FFIEC, GLBA, and DORA-related reviews do not start from stale exports, screenshots, and spreadsheets.

- Control and compliance context: Turns policy violations and posture findings into scoped work by showing which regulated assets they affect and whether the risk is open, remediated, or accepted.

- Financial data security context: Connects storage, database, log, backup, and cloud service records to data class, encryption state, compliance scope, and current control evidence when that context is maintained in the CMDB, tags, policies, or integrations.

- Vulnerability and remediation prioritization: Moves vulnerability work from severity-only triage to service-impact triage by tying findings to the affected asset, regulated workflow, and remediation path.